Bank on Hold As Housing Expected to Continue to Slow

January 18, 2017 by Adil Virani

Filed under Home Series, Latest News, Latest Rates, Mortgage FAQ, Recent News, Selling Your Home, Vancouver Mortgage Broker

Bank on Hold As Housing Expected to Continue to Slow

It is no surprise that the Bank of Canada maintained its target overnight rate at 1/2 percent today, reaffirming its view that the Canadian economy is still operating with considerable slack despite strong employment growth and inflation remains below the 2 percent target. The policy statement highlighted that that “uncertainty about the global outlook is undiminished, particularly with respect to policies in the United States.” Trump’s ascendancy to the highest office in the US portends major policy changes, some of which could have a direct impact on Canada.

For now, the Bank has chosen to incorporate assumptions about prospective tax policies only, resulting in a modest upward revision to its US growth outlook. US growth in 2017 was revised up only slightly, from 2.1 percent to 2.2 percent. The impact of the new administration’s fiscal stimulus is more pronounced in 2018, increasing the Bank’s forecast to 2.3 percent (up 0.3 percentage points from the October forecast). These are initial estimates, which include changes in tax policies only. Clearly, an important factor impacting Canada will be US trade policy. The impact of this and other fiscal measures will be updated in future Bank of Canada reports as more details become available.

The Bank’s forecast for US growth is above its estimate of the rate of potential US output expansion of about 1.8 percent in 2018. The economy is judged to be already at or near full capacity. Business investment in the US is expected to regain momentum as growth in demand remains above potential output.

Bond yields around the world, including here at home, have risen in anticipation of more stimulative fiscal policies and deregulation in the US, though financial conditions remain accommodative (Chart 1).

Global crude oil prices have recently averaged about 15 percent higher than assumed in the October Monetary Policy Report (MPR). By convention, the Bank is now assuming oil prices will remain at near current levels of $55 for Brent, $50 for West Texas intermediate and $35 for Western Canada Select. The Bank believes that the risks to this forecast remain tilted to the upside over 2017-18, since prices are still below levels likely required to support medium-term market rebalancing. The Bank’s new MPR, released today says that “the scope for sustained higher prices is limited, however, because technological advances have contributed to lower production costs for unconventional oil production, notably shale oil in the United States”. And the Trump administration supports the fracking sector.

Nevertheless, the worst is over for the Alberta economy, which we have already seen reflected in the housing sector, which has improved considerably in the most recent Canadian realtors report.

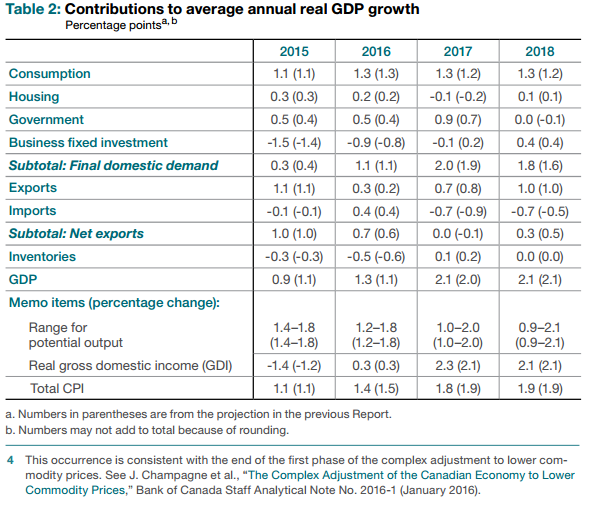

The Bank believes that growth in the Canadian resource-related sectors have troughed and investment and employment are being reallocated to the growing service sector. Real GDP in Canada is expected to grow at a rate moderately above potential output as housing slows. The Bank is estimating that housing boosted growth in 2015 and 2016 by 0.3 percent and 0.2 percent respectively. Housing will be a small net drain on activity this year, according to the MPR, reflecting the negative impact of tighter mortgage restrictions and the rise in mortgage rates (see Table).

Some have suggested that the Bank of Canada might cut interest rates again next year, particularly if housing slows too much. Judging from comments made by the CEO of the CMHC, a slowdown in housing is the intended result of the new rules. Clearly, Governor Poloz sees the enhanced mortgage stress tests and changes in the insurability of mortgages as mitigating his concerns of overextended homebuyers. It would take a material negative shock to growth for the Bank to cut rates.

On the other hand, others recently have suggested the Canadian economy will benefit sufficiently from the fiscal boom in the US for the Bank to hike rates by the end of this year. I believe this is unlikely as market rates have already risen and the potential negative impact of a stronger Canadian dollar on trade, as well as a potential US harder line on trade–such as recent US saber rattling on a border tax–will keep the Bank on the sidelines through the rest of this year.

Dr. Sherry Cooper

{kind=link}